Digital Payments: What Makes Adyen a Must-Watch Player?

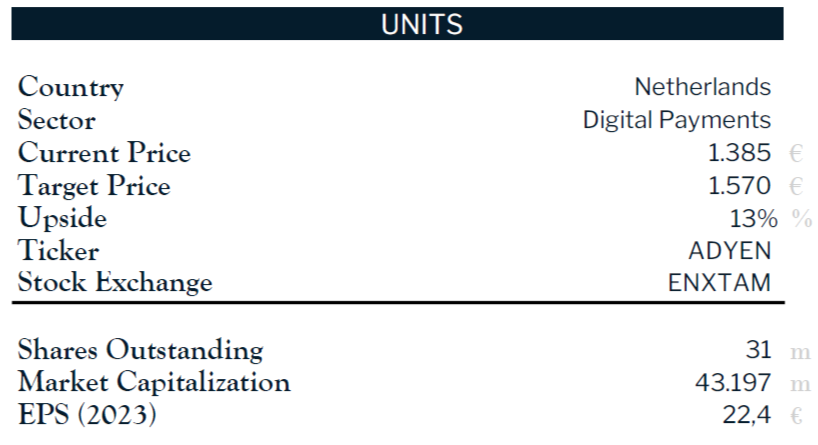

Equity Research: ADYEN N.V.

Summary

Introduction: Adyen, founded in 2006 in Amsterdam, is a global leader in digital payments, providing end-to-end solutions for online, in-person, and cross-channel transactions. The company has secured a reputation for reliability, innovation, and seamless integration, attracting major global clients like Spotify, Uber, and Microsoft.

Find our final recommendation and the link to the entire research at the end of the post.

Our recommendation rests on the following key elements of Adyen:

Customer Retention: over 80% of Adyen's revenue growth is driven by existing clients, supported by a churn rate below 1%.

Emerging Markets Positioning: investments in LATAM and APAC regions position Adyen for future growth as cashless transactions accelerate.

AI Integrations: tools like RevenueProtect and intelligent routing enhance transaction approval rates and minimize fraud.

Proprietary Technology: Adyen’s proprietary, in-house technology stack ensures efficiency, scalability, and innovation.

Business Model

Adyen's business is built on delivering a unified payment solution tailored for global merchants.

Business Segments:

Digital: supports e-commerce and subscription services by simplifying global payment complexities with single integration, intelligent routing, and RevenueProtect for fraud prevention, optimizing secure payment experiences.

Unified Commerce: integrates online and in-store transactions for seamless omnichannel shopping experiences, offering real-time insights and cross-channel services like in-store pickups and online returns.

Platforms: provides embedded payment solutions for marketplaces and SaaS providers with white-label services and the Embedded Financial Product (EFP) suite, enabling branded payments, split payments, and additional financial tools.

Geographic Reach:

EMEA: 55% of revenue, benefiting from a robust market presence.

North America: 25%, the fastest-growing market due to e-commerce expansion.

APAC: 15%, driven by mobile-first payment preferences.

LATAM: 5%, with strategic investments in key markets like Brazil and Mexico.

Company Strategy

Customer-Centric Expansion: deepening relationships with existing clients while acquiring new ones.

Proprietary Technology and Operational Efficiency: Adyen’s full control over its tech stack ensures speed, security and cost efficiency.

Geographic and Market Diversification: investments in underpenetrated regions drive long-term growth.

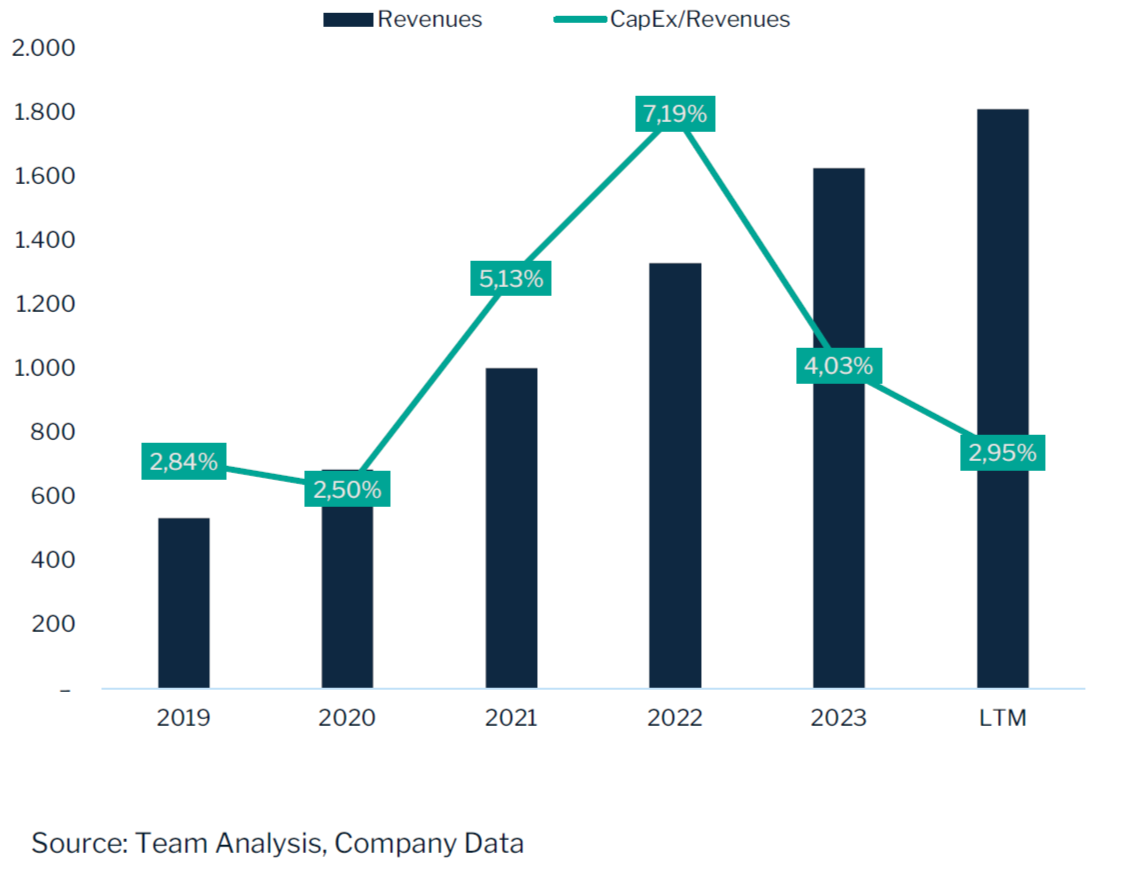

Financial Goals and Profitability: focused on achieving EBITDA margins exceeding 50% by 2026 while maintaining disciplined capital expenditures below 5% of net revenue.

Management

Adyen’s management team, led by co-CEOs Pieter van der Does and Ingo Uytdehaage, emphasizes sustainable growth, operational efficiency, and technological innovation.

Capital Allocation: Adyen prioritizes reinvestment in its proprietary platform, geographic expansion, and technological innovation while maintaining financial discipline.

Background and Compensation: Adyen’s executive team adopts a long-term approach to growth, eschewing short-term incentives for a structure rooted in equity ownership. This philosophy ensures alignment with shareholder value creation and fosters accountability.

Communication: Adyen maintains transparency with stakeholders by adhering to clear and open communication principles. This approach builds trust with merchants, regulators, and investors, ensuring alignment with the company’s strategic goals.

Sector Analysis

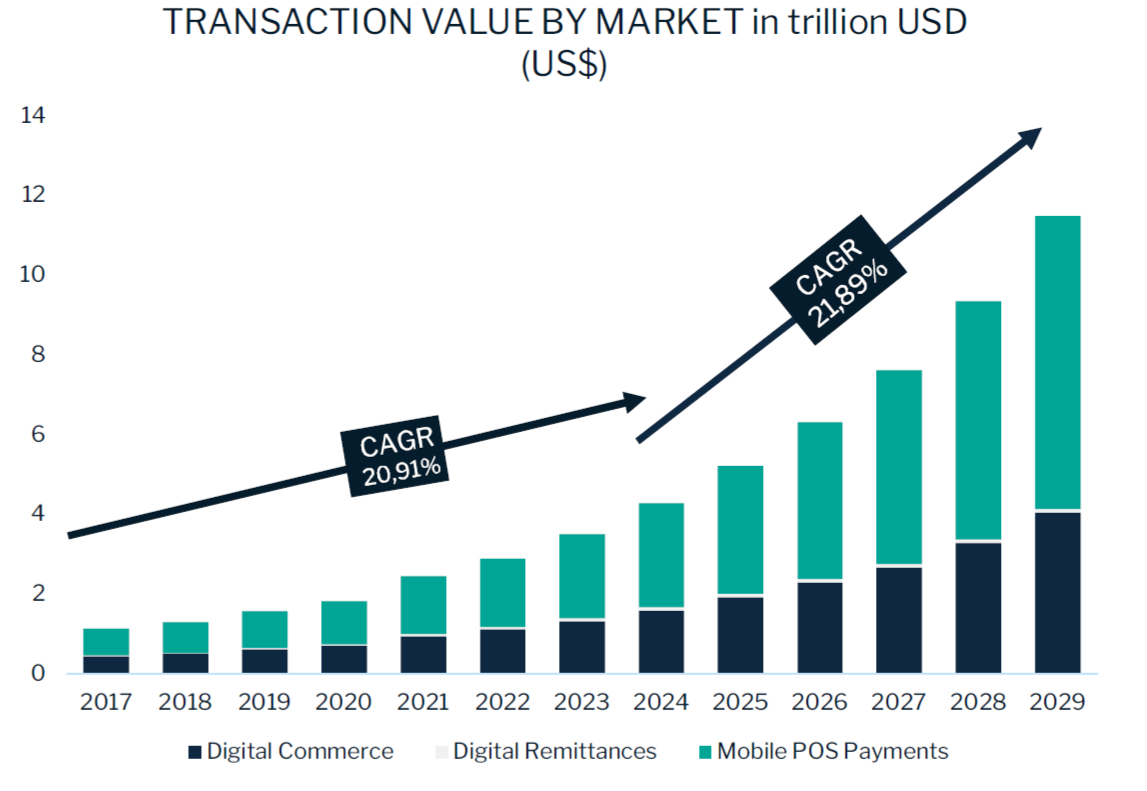

Digital Payments Market Growth: the digital payments market is projected to grow from €5.83 trillion in 2023 to €12.93 trillion by 2029, driven by e-commerce expansion, mobile payment adoption, and advances in AI-driven fraud prevention.

Digital Payments Industry Overview: Adyen operates in a dynamic and competitive industry, benefiting from macroeconomic shifts towards cashless transactions and rapid digital transformation. Its position as a global leader enables it to capitalize on growth opportunities while navigating competitive pressures.

External Analysis

SWOT Analysis

Porter’s Five Forces:

Power of Suppliers: Low, as Adyen’s proprietary technology reduces reliance on third-party providers.

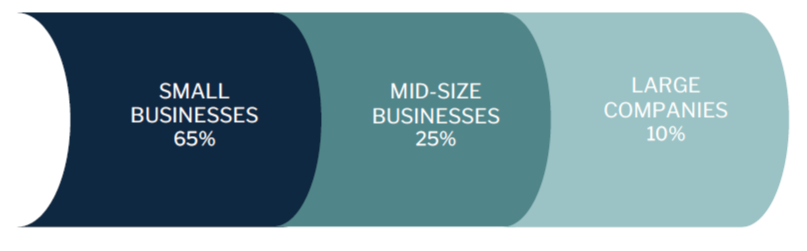

Bargaining Power of Customers: Moderate, with large enterprise clients having greater negotiating leverage.

Threat of New Entrants: Low, due to significant capital and regulatory barriers.

Threat of Substitutes: Moderate, with cheaper alternatives targeting smaller merchants but lacking Adyen’s integrated solutions.

Competitive Rivalry: High, with competition from PayPal and Stripe driving the need for continuous innovation.

Financial Analysis

Income Statement

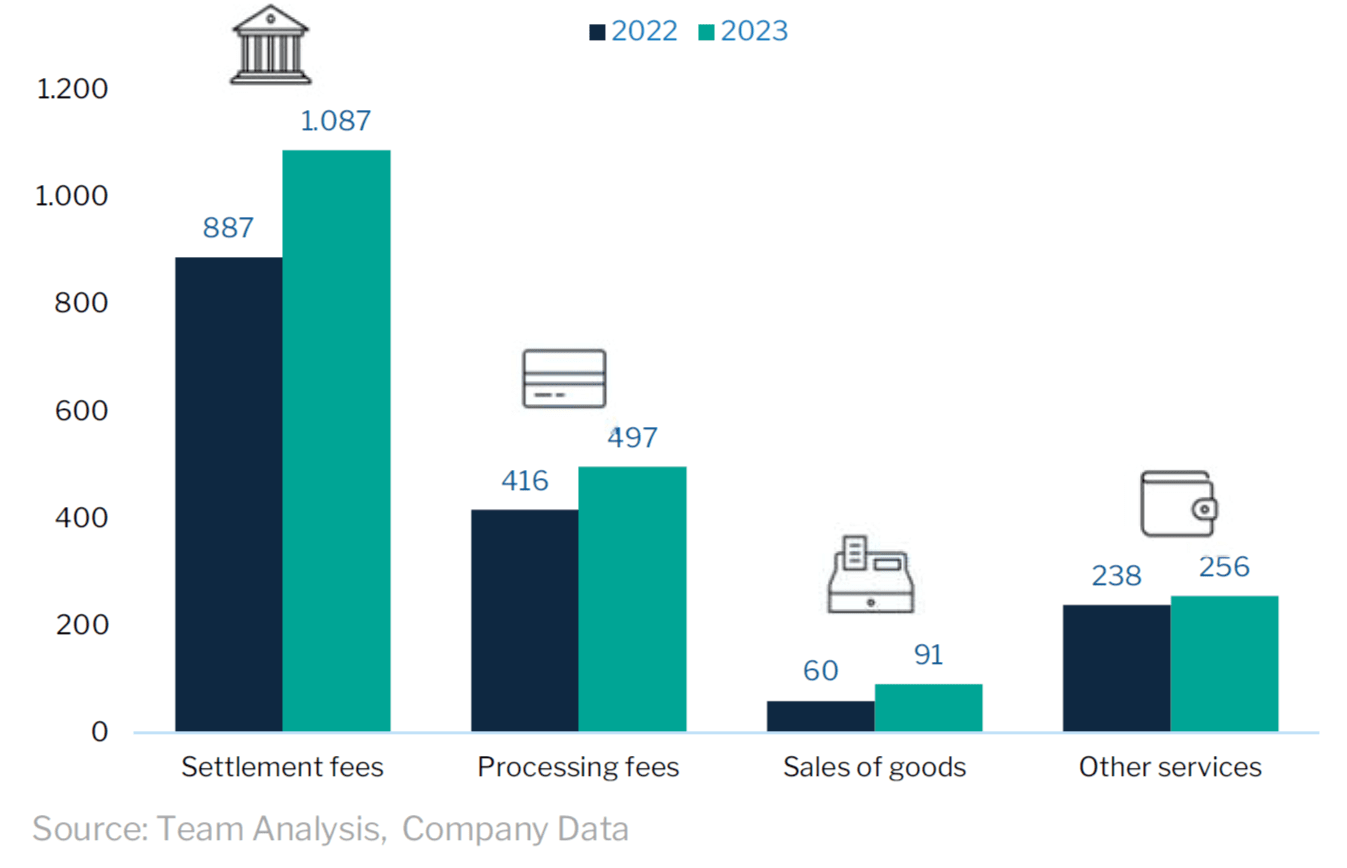

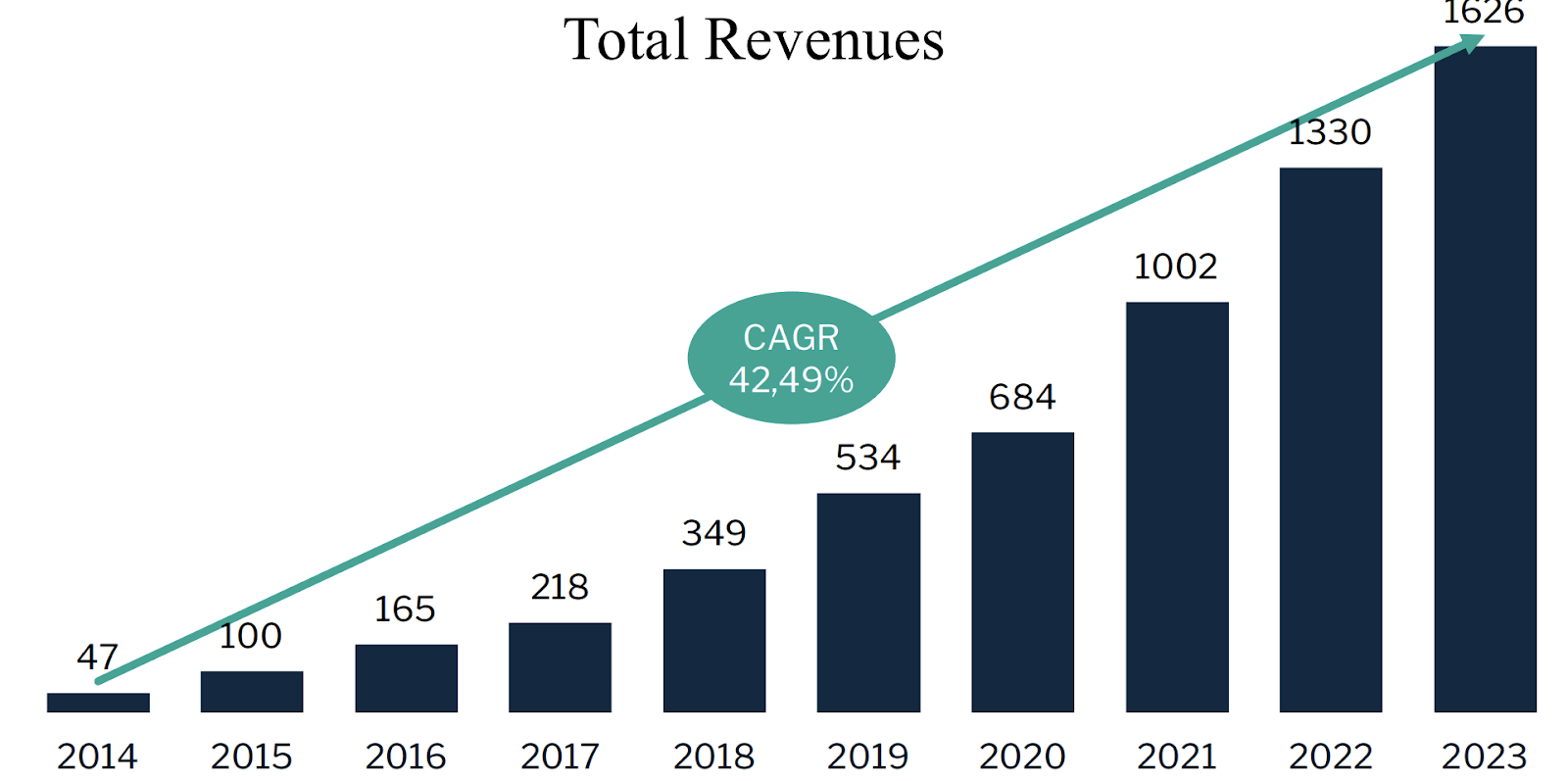

Adyen demonstrated robust revenue growth from 2014 to 2023, achieving a CAGR of approximately 25%. In 2023, net revenue reached €1.63 billion, a 22% increase from €1.33 billion in 2022.

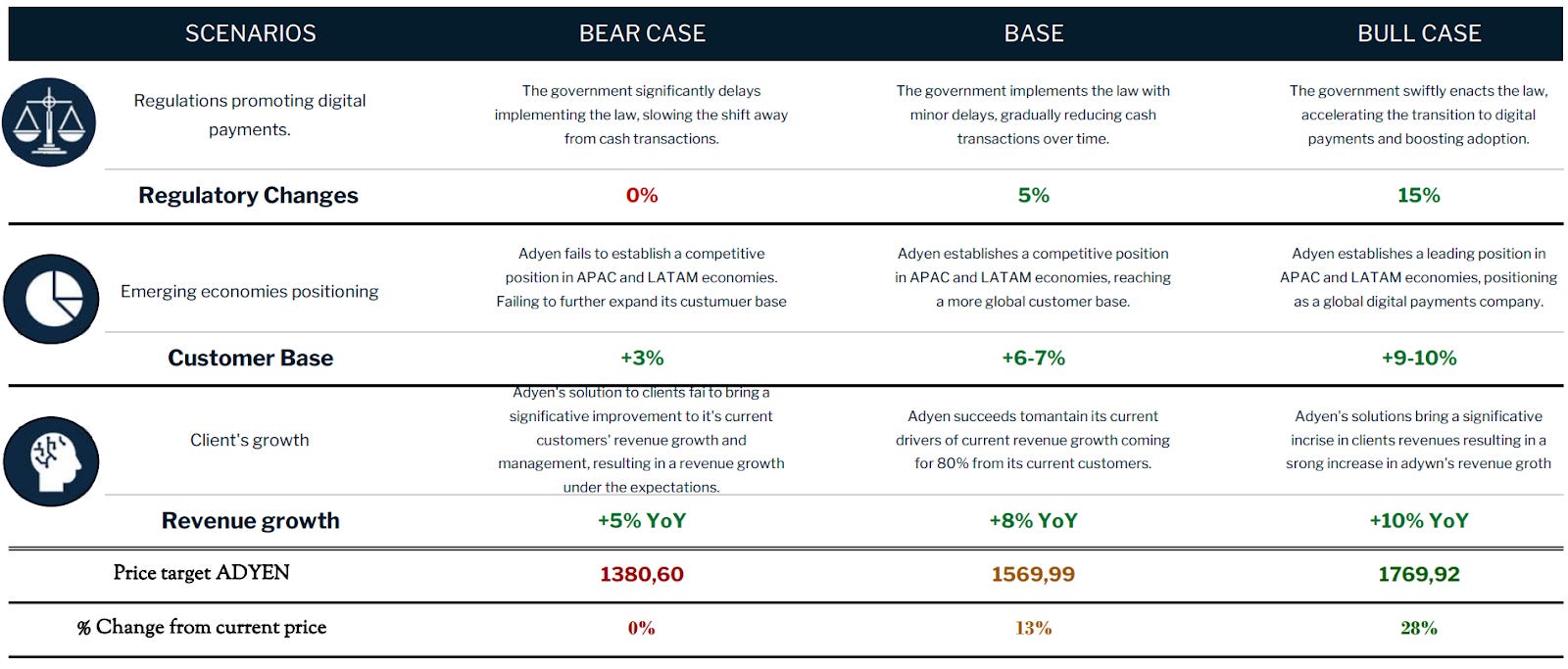

Future Growth Scenarios (2024-2028)

Base Scenario: 18% CAGR, reaching €3.05 billion in revenue by 2028.

Pessimistic Scenario: 12% CAGR, revenue reaching €2.6 billion by 2028.

Optimistic Scenario: 22% CAGR, achieving €3.6 billion by 2028, driven by penetration in underserved markets and AI-driven solutions.

Margins

Gross Profit Margin: 89% in 2023, supported by operational efficiency and pricing power.

EBITDA Margin: 61% in 2023, reflecting disciplined cost management and scalability.

Net Income Margin: 27% in 2023, underscoring strong profitability and effective cost controls.

Free Cash Flow Margin: 32% in 2023, highlighting Adyen’s ability to generate liquidity for reinvestment and shareholder returns.

ROE (Return on Equity): ROE grew from 9% in 2015 to a stable 25% in 2023, with peaks at 31% in 2019 and 2021, driven by exceptional profitability and balanced equity growth.

ROIC (Return on Invested Capital): ROIC stabilized at 6% in 2023, supported by NOPAT (Net Operating Profit After Tax) Margin growth from 12% in 2015 to 27% in 2023 and an increase in Capital Turnover from 0.9x to 1.9x over the same period.

EPS (Earnings Per Share): EPS grew from €6.0 in 2019 to €11.8 in 2023, with a Compound Annual Growth Rate (CAGR) of 14.52%. Projections indicate EPS will reach €19.6 by 2028, growing at a 10.14% CAGR.

ROA (Return on Assets): ROA increased from 5% in 2015 to 8% in 2023, reflecting efficient asset utilization. It is expected to potentially reach 21% by 2028, driven by further geographic and operational expansion.

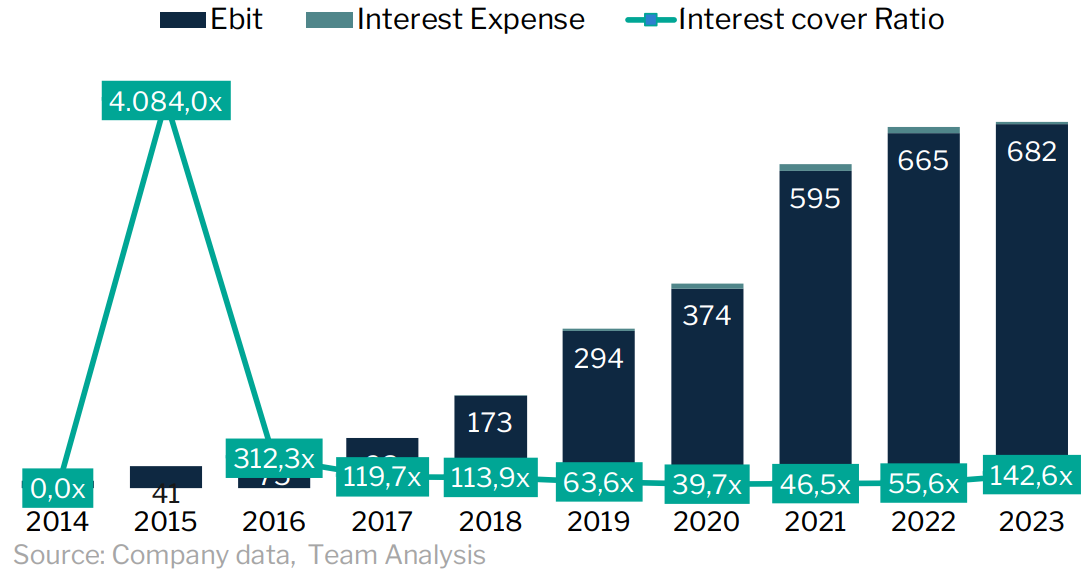

Balance Sheet

Interest Cover 0.1x

Debt-to-free cash flow 4.9x

Quick Ratio 1.4x

Valuation

We use two models to look at the valuation of a company:

Discounted Cash Flows Analysis (DCF)

Relative valuation

DCF

WACC: 8,39%

Terminal growth rate to stabilize at 2,5% after 2028

EV/EBITDA multiple of 19,4x

Relative Valuation

Target Price: $1,395 (Upside of 7.8%).

EV/EBITDA: 22.9x

The multiples valuation for Adyen supports the findings from cash flow and DCF analysis. The comparison included peers like PayPal and Stripe, whose business models are similar but on a smaller scale, resulting in lower multiples. Larger companies, such as Visa and Mastercard, offered more relevant benchmarks, highlighting Adyen's robust margins and economies of scale, which justify its premium valuation.

Investment Risks

Strategic and Competitive Risks

Intense competition and price pressures may impact margins.

Challenges in scaling product offerings or adapting to regional markets.

Global expansion and regulatory integration risks could hinder growth.

Cybersecurity and Operational Risks

Reliance on in-house technology centralizes risks of failures and cyberattacks.

Disruptions in global partnerships or supply chains may harm revenues.

Talent retention is critical for maintaining innovation and efficiency.

Regulatory and Financial Risks

Non-compliance with global regulations, such as GDPR, could result in fines.

Currency fluctuations and economic instability in international markets pose risks.

Tiered pricing strategy creates variability during economic downturns.

General Risks

Economic pressures and geopolitical tensions affect transaction volumes.

Stock market volatility impacts valuation and investor confidence

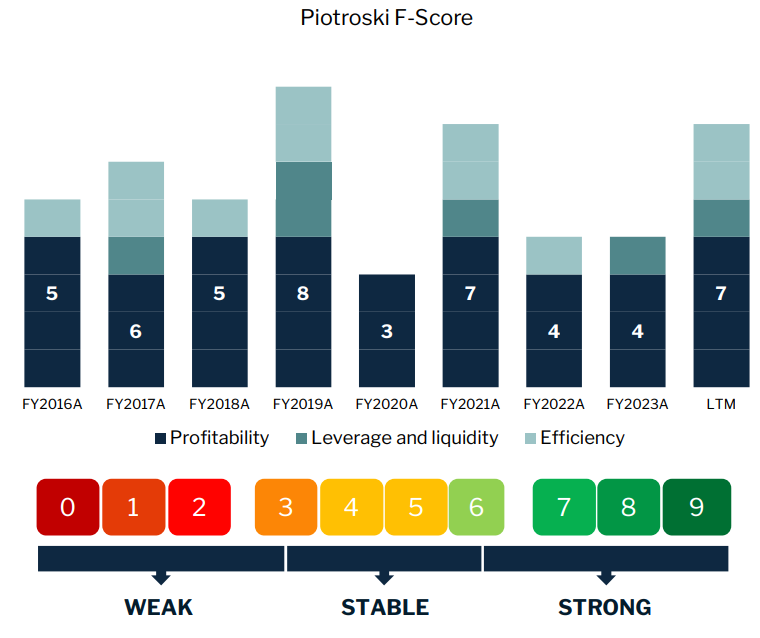

The Piotroski F-Score

The Piotroski F-Score is a tool used to assess a company's financial health based on nine criteria across three categories: profitability, operational efficiency, and capital structure.

Adyen Piotroski F-Score in 2023 is within the optimal range of 7 to 9

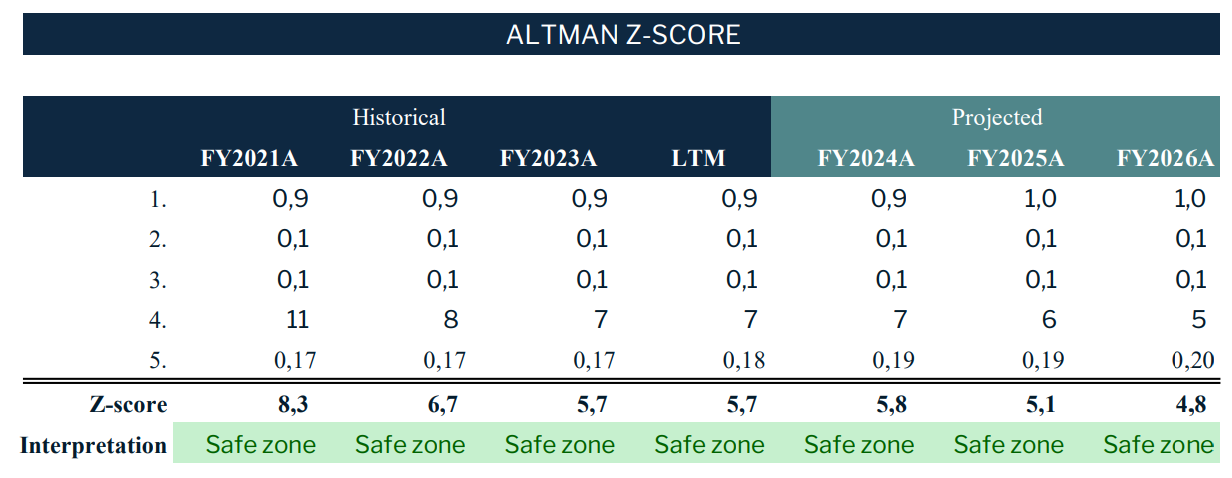

The Altman Z-Score

The Altman Z-score is a financial metric that predicts a company's insolvency risk within two years.

Based on our analysis, the company is in a safe zone, with a low risk of default in the short to medium term.

Final recommendation: We issue a BUY recommendation for Adyen with a one-year target price of €1556, presenting a 22% upside potential from ADYEN's closing price of €1277 on November 17th, 2024.

You can access the full research here.