Is Adobe a High-Quality Company?

Equity Research: Analysis of Adobe Incorporate.

Summary

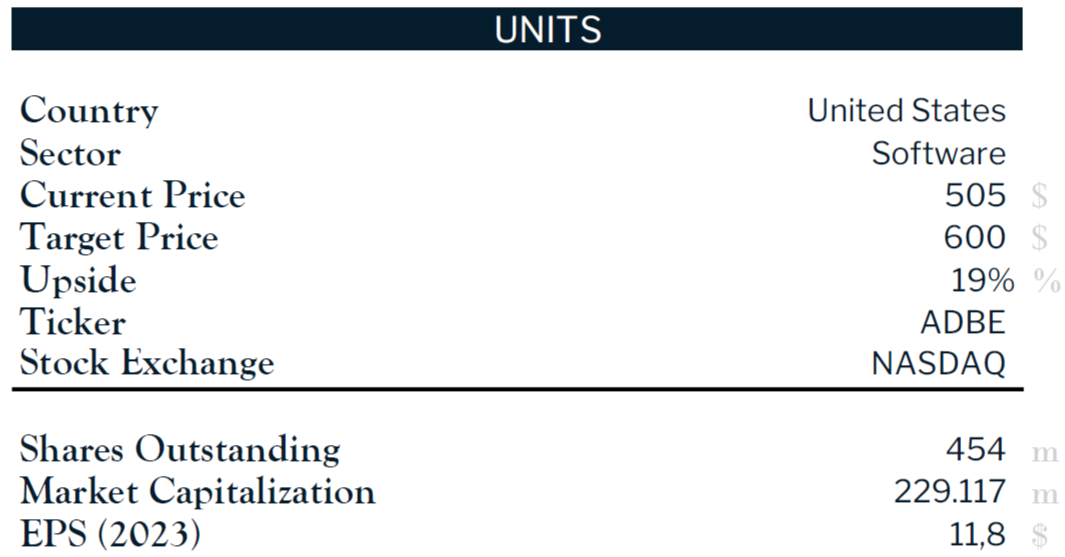

Investment Summary: we issue a BUY recommendation for Adobe with a one-year target price of $541.39, presenting an 11% upside potential from ADBE's closing price of $487 on November 1st, 2024. The target price is based on a Discounted Cash Flow (DCF) method and supported by Relative Valuation.

Our recommendation rests on the following key catalysts:

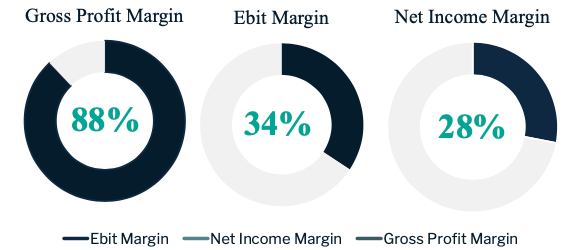

Adobe’s Technology and Ecosystem Moat: Adobe's Creative Cloud ecosystem offers unmatched integration and advanced tools for digital creativity, creating high switching costs for professionals. The SaaS model ensures recurring revenue, high margins (88% gross profit, 28% net income), and resilience to economic cycles.

Excellent Positioning to Lead the Generative AI Trend: Adobe is poised to lead in generative AI with innovative tools like Adobe Firefly, which outperform competitors and integrate seamlessly into popular applications like Photoshop and Illustrator.

Growth-Oriented Vision: Adobe allocates 17.5% of its revenue to R&D, balancing organic growth with strategic acquisitions like Frame.io and Workfront. Its management focuses on long-term value, consistently introducing innovative tools and expanding its offerings.

Market Leader in the Professional Creative Software Industry: the global creative software market has grown steadily, with a 5.13% CAGR in recent years, though projected to slow to 1.77% CAGR through 2029. Adobe, the market leader, is well-positioned to benefit, driven by its advanced tools and 2023's 17% global growth in design products.

Business Model

Business Segments:

Digital Media

Digital Experience

Publishing and Advertising

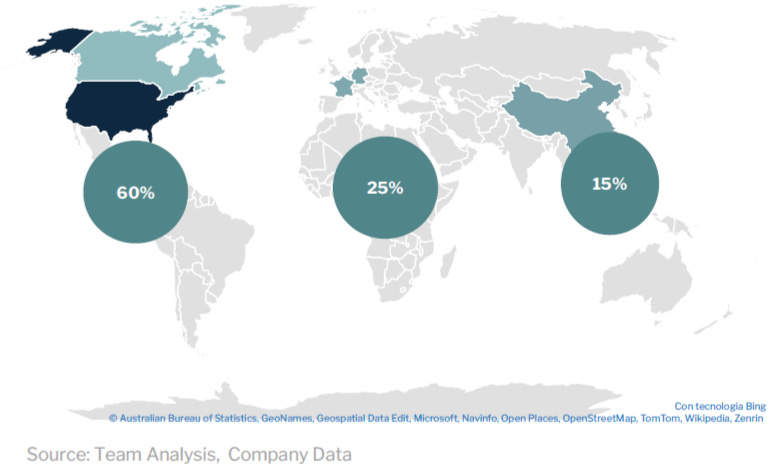

Geographic Reach: Adobe operates globally, with key markets in North America, Latin America, EMEA (Europe, Middle East, and Africa), and APAC (Asia-Pacific). The United States accounts for a significant portion of its revenue.

Company Strategy:

Transformation to SaaS: in 2012, Adobe transitioned its core products, such as Photoshop, Illustrator, and Premiere, from a traditional software license sales model to a cloud-based subscription model called Adobe Creative Cloud. This strategic shift primarily resulted in recurring revenue and a flexible pricing structure.

Strategic Acquisitions

Global Expansion

Adobe offers a wide range of software solutions across three main areas:

Creative Cloud: tools for photo and video editing (Photoshop, Lightroom, Premiere Pro, After Effects), graphic design (Illustrator, InDesign), generative AI (Firefly), and social content creation (Express).

Document Cloud: solutions for PDF management and digital documentation, including Adobe Acrobat, Acrobat Reader, Acrobat Sign, and Adobe Scan, offering features like editing, e-signatures, and mobile optimization.

Marketing and Commerce: platforms for managing digital experiences (Experience Manager, Commerce), customer journeys (Campaign, Journey Optimizer), and marketing automation (Marketo Engage), supported by AI for personalization and workflow optimization (Workfront, Target).

Management

Capital Allocation: Adobe's management excels in capital allocation, balancing investment in growth with financial solidity. A Quick Ratio of 1.3 (2023) reflects strong financial health, allowing substantial reinvestment. The company's 17% revenue allocation to R&D, as mentioned before, highlights its commitment to innovation, while acquisitions like Frame.io, Workfront, and the attempted Figma purchase focus on high-growth opportunities. Share buybacks, including the 2022 program during a market correction, reflect management's confidence and dedication to shareholder value.

Background and Compensation:

Experienced Leadership: CEO Shantanu Narayen, with Adobe since 1998 and CEO since 2007, has driven innovation and growth, including the transformation to a cloud-based subscription model.

Internal Promotion: Many leaders have risen through Adobe's ranks, fostering a deep understanding of operations and strategy.

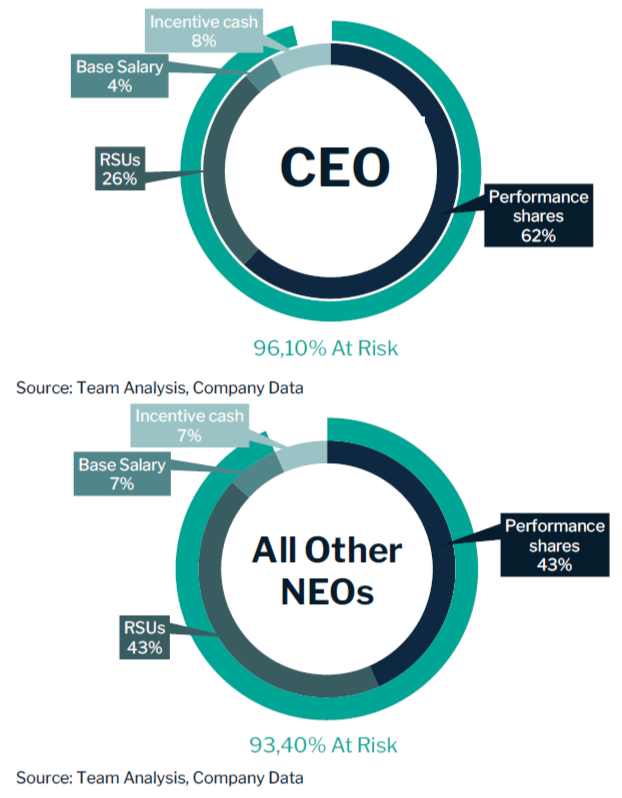

Aligned Incentives:

Over 90% of executive compensation is tied to company performance and stock growth.

Compensation tools like RSUs and Performance Shares link pay to long-term goals and financial success.

This structure encourages sustainable, strategic decision-making over short-term gains.

Focus on Long-Term Value: Adobe's leadership is incentivized to prioritize shareholder value and ensure continued growth and innovation.

Sector Analysis

Software Market Growth:

The global software market grew significantly in 2023, with Artificial Intelligence (AI) leading at 39% growth, far outpacing Design (17%) and Marketing, HR, and Security (14% each).

AI's growing importance drives innovation in creative software, automating and enhancing processes like design, video editing, and content production.

Creative Software Industry: the global creative software market has grown steadily (CAGR 5.13%) and is projected to expand more slowly through 2029 (CAGR 1.77%). These tools, essential for creating and managing digital content are increasingly critical across industries such as entertainment, marketing, and advertising. Demand surged during the COVID-19 pandemic due to accelerated digitization.

Growth Factors:

Rising demand for visual and multimedia content from social platforms and e-commerce.

Increased adoption of tools for hybrid and remote work models.

Continuous innovation in AI, automation, and cloud collaboration.

Slowing Factors:

Market saturation, reducing new customer opportunities.

Competitive pressure from open-source and low-cost solutions.

External Analysis

SWOT Analysis

Strengths:

Market leadership in creative software. Diversified product portfolio.

Strong brand and customer loyalty.

Subscription-based business model.

Significant investments in AI and machine learning.

Weaknesses:

Dependence on creative and marketing sectors, which could be vulnerable to economic downturns.

Relatively high prices for products.

Increasing competition in creative software and digital marketing.

Opportunities:

Expansion into emerging markets.

Strategic acquisitions to strengthen presence in key sectors.

Growth driven by global digitalization.

Accelerated adoption of cloud computing and SaaS services.

Threats:

Aggressive competition from new tech players and more accessible platforms.

Regulatory changes regarding data privacy.

Macroeconomic risks, such as recessions or currency fluctuations.

Software piracy.

Porter’s Five Forces:

Power of Suppliers: Low. Adobe develops most software in-house, reducing dependency on external vendors. While reliant on cloud platforms like AWS and Azure, Adobe's size and ability to switch suppliers give it strong negotiating power.

Bargaining Power of Customers: Moderate. Professional users and enterprises are locked into Adobe's ecosystem due to its advanced integration, but large companies can negotiate better terms. Amateur users can switch to cheaper alternatives.

Threat of New Entrants: Low. High barriers to entry include significant investment in technology and difficulty replicating Adobe's ecosystem, user base, and innovation.

Threat of Substitutes: Moderate. Alternatives like Canva cater to non-professionals, and competitors like DocuSign and Google Docs exist in document management. However, Adobe's tools remain essential for professionals and enterprises needing advanced features.

Competition: High. Adobe faces competition from Figma in collaborative design, Salesforce in digital marketing, and Canva for non-professionals. Despite this, Adobe retains an edge with its integrated product ecosystem and longstanding leadership.

Financial Analysis

Income Statement

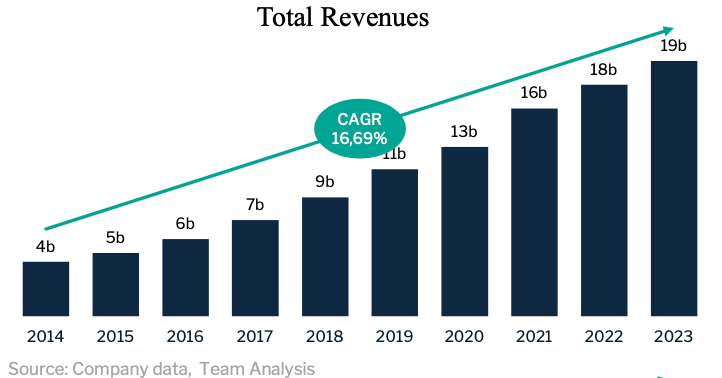

From 2014 to 2023, Adobe demonstrated resilient and sustained revenue growth, with no year-over-year decline, achieving an average YoY growth of 18.8% and a CAGR of 16.69%.

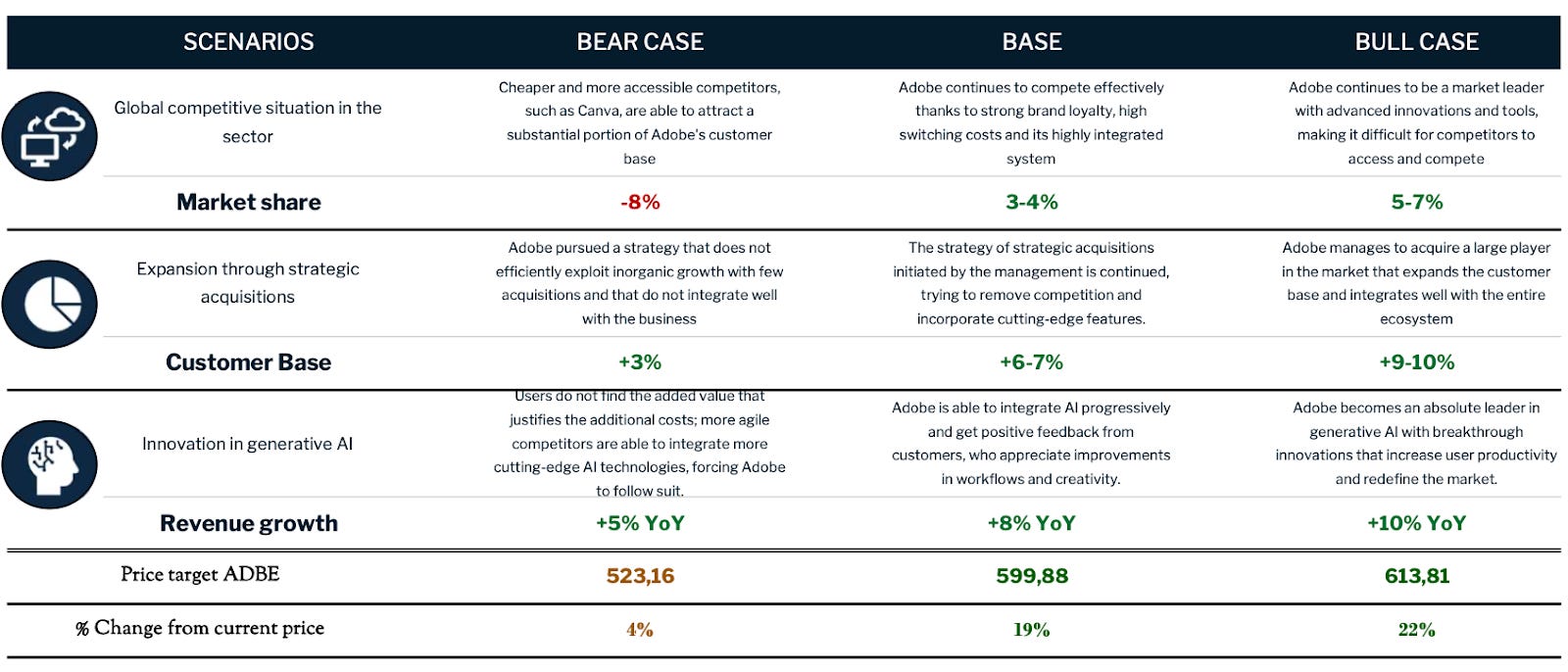

Future Growth Scenarios (2024-2028)

Base scenario: Adobe is projected to maintain steady revenue growth with an estimated 8.3% CAGR from 2024 to 2028, reaching $28.49 billion by 2028.

Pessimistic Scenario: Adobe's revenue growth slows to a 7.1% CAGR, reaching $27.372 billion by 2028 due to competition from lower-cost alternatives. While new customer acquisition may lag, Adobe's strong brand reputation and loyal user base are expected to maintain its dominant market position.

Optimistic Scenario: Adobe leverages innovations to boost subscriptions and renewal rates, achieving a 9.8% CAGR and $30.907 billion in revenue by 2028, solidifying its market leadership.

Margins

Thanks to its transition to the SaaS (Software as a Service) model, Adobe has significantly impacted its profit margins.

Gross Profit Margin grew from 84.9% in 2014 to 88.7% in 2023.

The EBITDA margin increased from 17.9% in 2014 to 38.8% in 2023.

The Net Income Margin grew from 6.5% in 2014 to 27.9% in 2023.

Quality Profit Ratio reached 109% in 2023.

The EPS has grown robustly from 6.0 in 2019 to 11.8 in 2023, with a Compound Annual Growth Rate (CAGR) of 14.52%.

The ROA has generally shown an upward trend from 6% in 2015 to 19% in 2023

ROE grew significantly from 9% in 2015 to 36% in 2023.

Balance Sheet

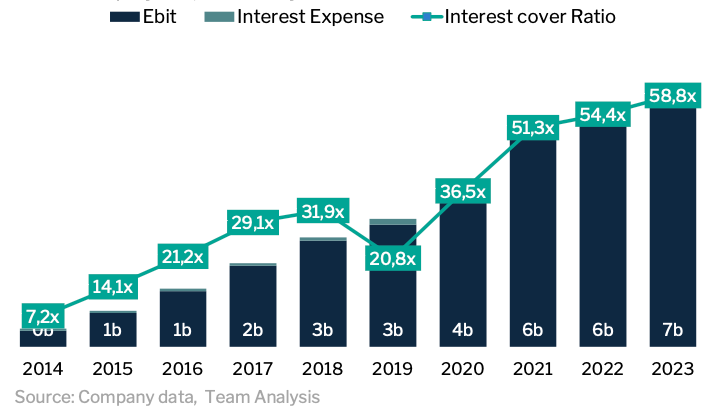

Interest Cover ratio 51.2x

Free cash flow to debt 0.6x

Quick ratio 1.2x

Valuation

We use two models to look at the valuation of a company:

Discounted Cash Flows Analysis (DCF)

Relative valuation

DCF

WACC: 9.52%

Terminal growth rate stable at 4% after 2028

EV/EBITDA of 32.5x

Relative Valuation

Target price of $520 (6.9% upside).

EV/EBITDA, averages 27x for Adobe versus 23.6x for peers, reflecting its competitive edge.

Adobe’s P/E ratio of 41.2x, below the sector average of 45x, suggests moderate undervaluation despite strong growth expectations.

Investment Risks

1) Risks Related to Adobe's Ability to Grow the Business

Adobe must continually innovate to sustain growth and market leadership, facing challenges such as ethical concerns with AI, integration of acquisitions, and competition from low-cost products. Failure in these areas could damage customer trust, financial performance, and brand reputation, threatening long-term success.

2) Risks Related to Adobe's Ability to Manage Operational Aspects of the Business

Operational risks include reliance on third-party IT systems, cyber threats, and data breaches, which may harm Adobe’s reputation and incur costs. Disruptions from partners, suppliers, inflation, and political instability could affect sales and raise expenses. Retaining talent amid high competition and navigating complex sales cycles are also key challenges.

3) Risks Related to Laws and Regulations

Global expansion exposes Adobe to compliance risks with data privacy laws and regulatory changes, such as the EU-U.S. Safe Harbor revocation. Non-compliance by Adobe or its partners, particularly in emerging markets, could result in penalties and operational issues.

4) Risks Related to Financial Performance

The subscription-based revenue model creates short-term variability, with risks from slower renewals or sign-ups impacting cash flow. Adobe faces foreign exchange risks despite hedging, and its debt obligations, including unsecured notes and a credit line, heighten exposure to financing costs and reduce financial flexibility.

5) General Risk Factors

Economic and political instability in global markets could reduce customer spending and delay purchases. Adobe's success relies heavily on retaining skilled employees in a competitive industry. Stock market volatility, driven by competitor actions, analyst expectations, and global events, could also affect valuation and investor confidence.

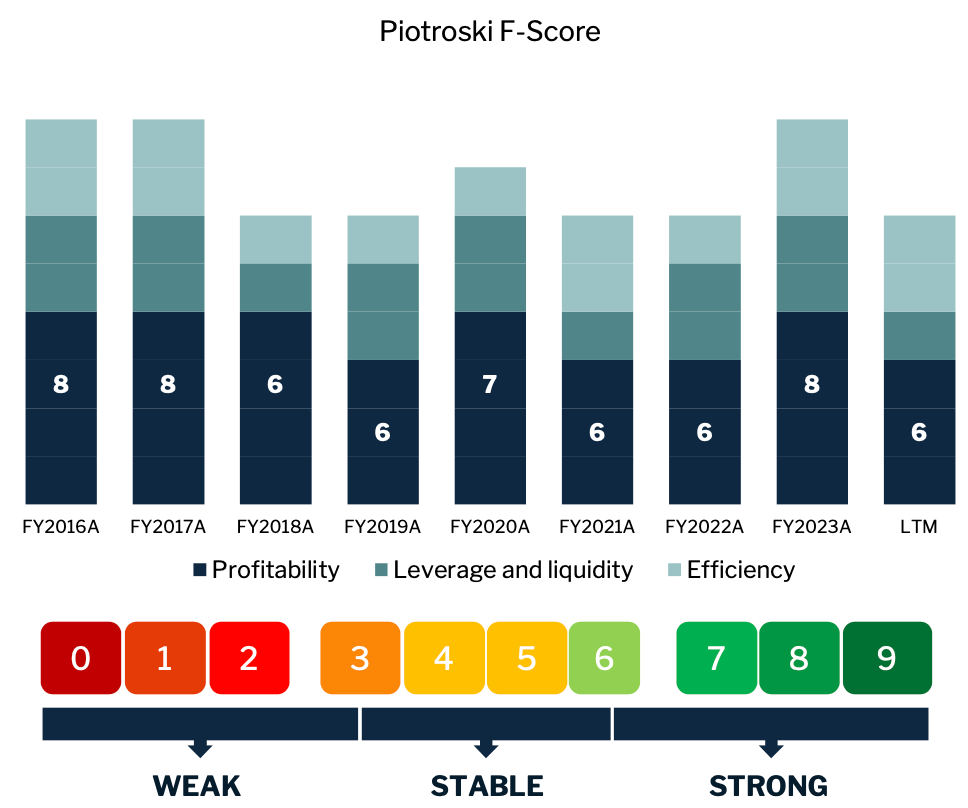

The Piotroski F-Score

The Piotroski F-Score is a tool used to assess a company's financial health based on nine criteria across three categories: profitability, operational efficiency, and capital structure.

Adobe’s F-Score in 2023: 7-9, optimal range

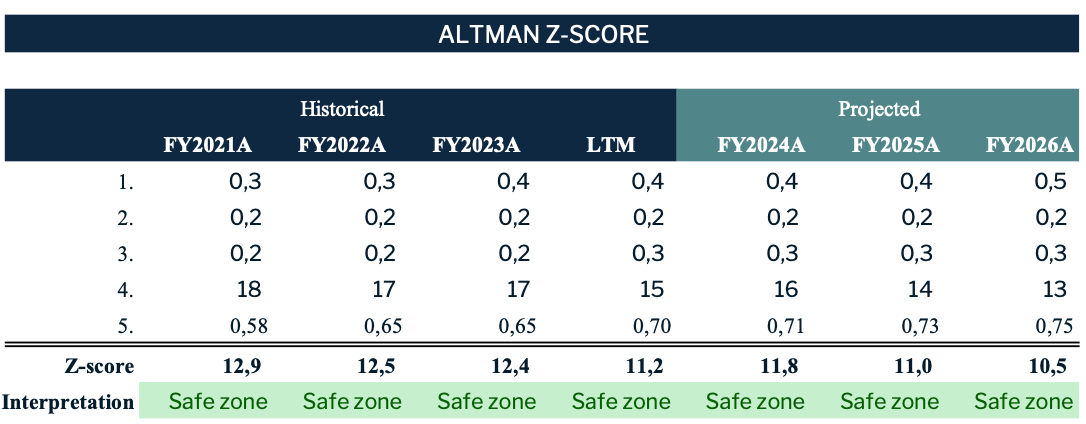

The Altman Z-Score

The Altman Z-score is a financial metric that predicts a company's insolvency risk within two years.

The company is in a safe zone, with a low risk of default in the short to medium term.