Is Microsoft the Ultimate Investment?

Equity Research: Analysis of Microsoft Corporation Inc.

Summary

Find our final recommendation and the link to the full research at the end of the post.

Our recommendation rests on the following key elements of Microsoft:

Great Leader in a Great Position: Microsoft is a global leader in technology, excelling in software, cloud computing, AI, gaming, and hardware.

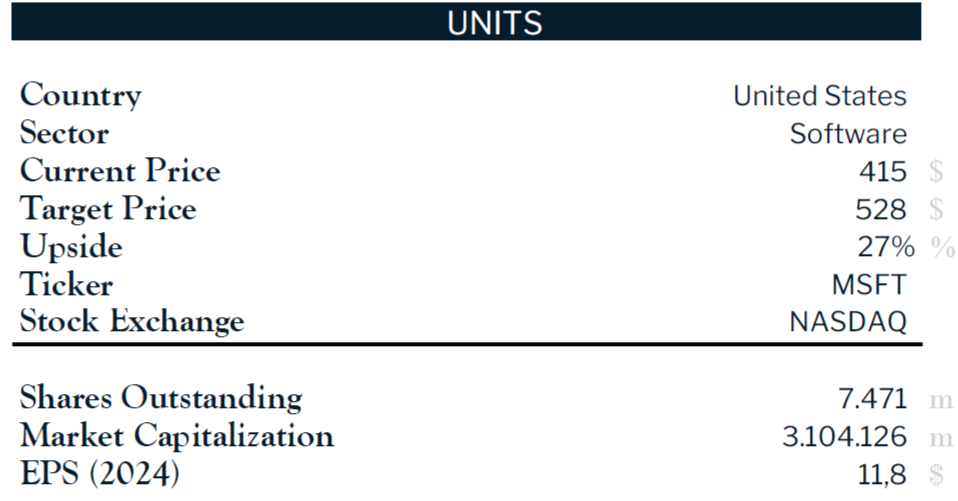

Biggest Software Company: Microsoft is the largest software company globally with a $3.1T market cap.

A Progressively Digitized World: the world is increasingly digitized, with booming e-commerce ($6.3T in 2024), 5.7 billion internet users, 20% growth in cloud demand, and a 28.46% AI market CAGR by 2030.

Core Business Segments: Productivity and Business Processes, Intelligent Cloud, and More Personal Computing.

Business Model

Business Segments:

Productivity and Business Processes

Intelligent Cloud

More Personal Computing

Geographic Reach: Microsoft's revenue distribution is heavily centered in the Americas (55%), with APAC and EMEA contributing 25% and 20%, respectively. The U.S. leads with 50% of total revenues, followed by China (20%) and the UK (12%).

Company Strategy

Microsoft’s strategy is rooted in its mission: "empower every person and every organization on the planet to achieve more".

Key components include:

Customer Base: spanning businesses, institutions, and individuals, with businesses and institutions generating the main share of revenue.

Global Markets

Strategic Investments: targeted spending in AI, gaming, and cloud services.

Distribution Channels: robust network including OEMs, enterprise sales, online platforms, and retail outlets.

Security: heavy investment in cybersecurity.

Acquisitions and Partnerships: high-profile deals like Activision Blizzard and OpenAI.

Microsoft’s holistic approach highlights its ability to adapt and innovate, setting the standard for the modern tech landscape.

Productivity and Business Processes

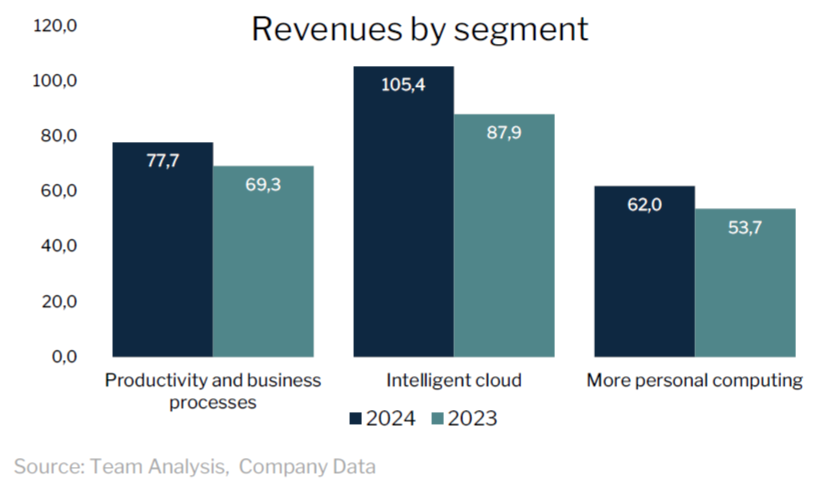

The Productivity and Business Processes segment generated $77.7 billion in 2024. Anchored by widely-used tools like Office and LinkedIn, this segment excels in workplace productivity.

This segment also overlaps with Microsoft’s Intelligent Cloud initiatives, which offer:

Server Products and Cloud Services: platforms like Azure and GitHub that enhance IT productivity.

Enterprise and Partner Services: strategic consulting and support for deploying Microsoft’s solutions.

Intelligent Cloud & AI

Microsoft’s Intelligent Cloud segment, centered around Azure, contributed $105.4 billion in revenue in 2024.

The company’s strategic partnership with OpenAI exemplifies its AI leadership:

2019: $1 billion investment in OpenAI to train large language models on Azure.

2023: A $10 billion multi-year investment, solidifying Azure as the exclusive platform for OpenAI and driving AI integration into Microsoft 365.

Innovations like Microsoft 365 Copilot embed AI across segments, from productivity tools to cloud computing, giving Microsoft a clear competitive edge.

More Personal Computing

In 2024, Microsoft’s More Personal Computing segment generated $62.4 billion, its lowest revenue contributor but vital to the company’s identity. Key highlights include:

Windows and Copilot

Gaming

Devices

Search Engine and Browser

Microsoft’s ability to integrate software, gaming, and hardware creates a cohesive ecosystem that resonates with both enterprise and retail customers.

Management

Capital Allocation: in 2024, Microsoft invested $29.5 billion in R&D. Key moves like the Activision Blizzard acquisition and OpenAI partnership, along with strong shareholder returns, reflect its dominance.

Leadership & Compensation: Microsoft’s leadership, led by CEO Satya Nadella, CFO Amy Hood, and President Brad Smith, drives transformation and stability. With 95% of the CEO’s pay tied to performance, executive compensation aligns with shareholder interests and growth.

Main Shareholders: institutional investors hold 71% of Microsoft’s shares, led by Vanguard (8.95%), BlackRock (7.30%), and State Street (4%). Insiders own 6.2%.

Sector Analysis

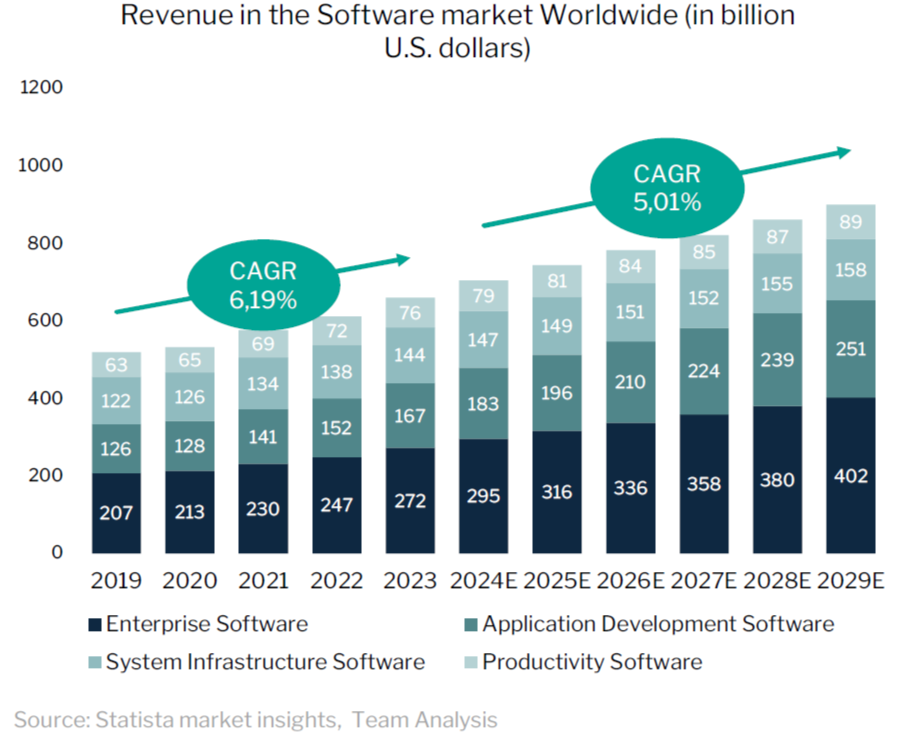

Software Market Growth: the software industry is experiencing rapid growth. With a projected 5.01% CAGR from 2024 to 2029, the market is set to reach $896 billion. Microsoft is well-positioned to capitalize on digitalization and advancements in AI and cloud technologies.

The industries driving today’s digital world are:

Productivity

Cloud Computing

Personal Computing

Microsoft seamlessly integrates these industries with its ecosystem of Microsoft 365, Azure, and Surface devices, showcasing leadership and synergy across all three sectors.

External Analysis

SWOT Analysis

Porter’s Five Forces

Power of Suppliers: Moderate. Microsoft depends on suppliers like Nvidia for GPUs, critical for AI and data centers.

Bargaining Power of Customers: Low. Microsoft’s broad customer base and dominance in operating systems and productivity tools result in high switching costs.

Threat of New Entrants: Low to Moderate. high capital requirements, brand loyalty, and Microsoft’s established ecosystem make entry challenging.

Threat of Substitutes: Moderate. competitors like Google Workspace and AWS offer alternatives in productivity and cloud services.

Competitive Rivalry: High. rivalry is intense, with Amazon, Google, Apple, and Salesforce competing across core segments. AWS leads in cloud, and Google Workspace challenges Office.

Financial Analysis

Income statement

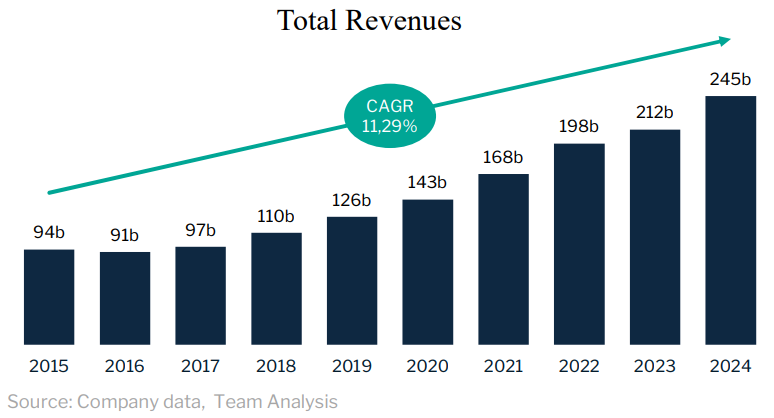

Microsoft grew steadily from 2015 to 2024, with a 10.7% YoY growth average and a 14.3% CAGR since 2019.

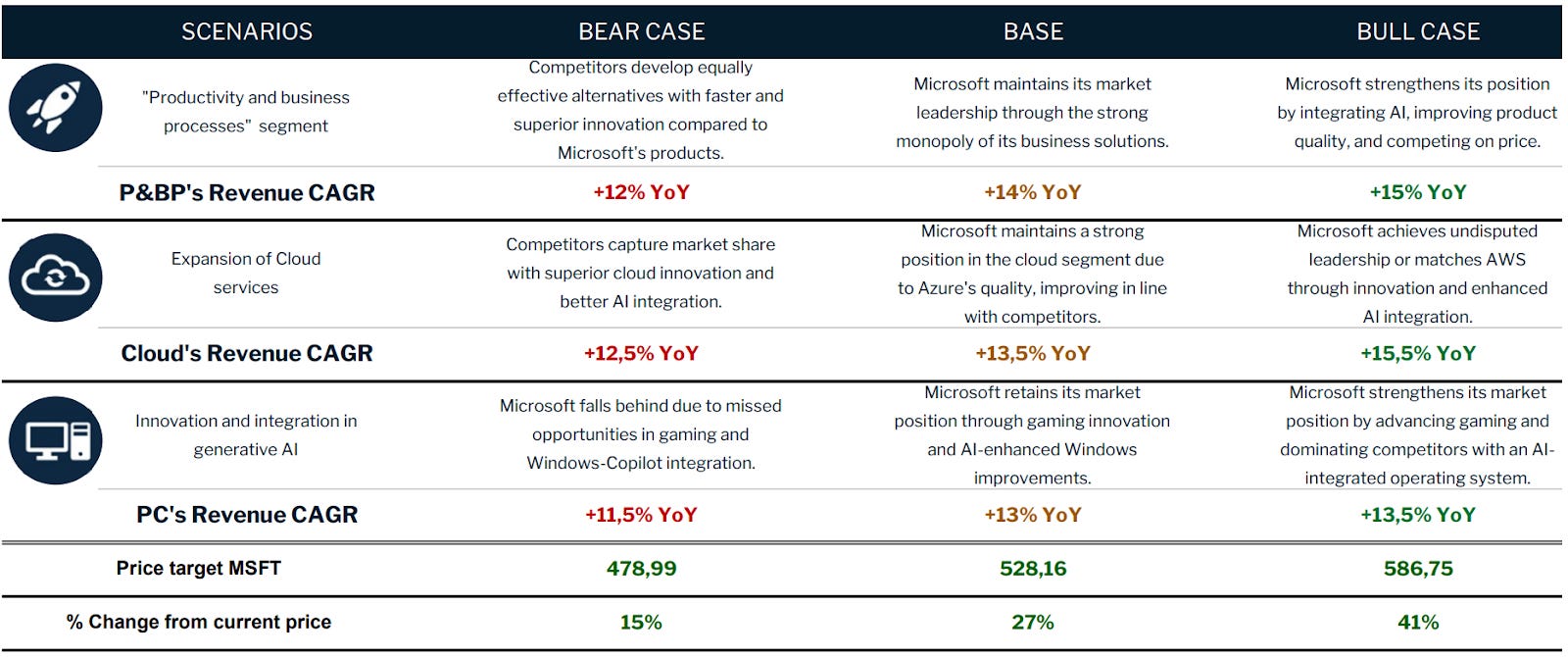

Future Growth Scenarios (2025-2029)

Base Scenario: 12.4% CAGR, $444B revenue by 2029.

Pessimistic: 10.9% CAGR, $415B revenue by 2029.

Optimistic: 13.67% CAGR, $468B revenue by 2029.

Margins

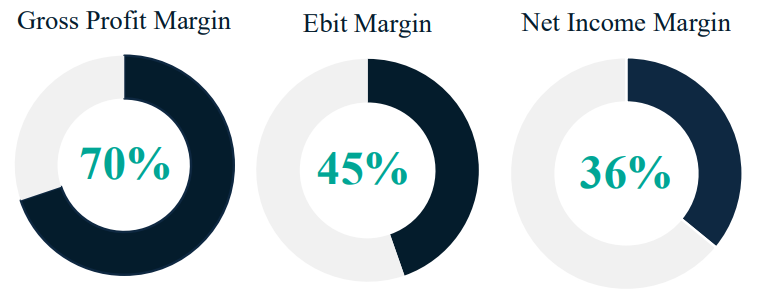

Microsoft has steadily increased profit margins, leveraging the software industry's scalability for high profitability.

The Gross Profit Margin has shown a steady upward trend, increasing from 65% in 2018 to 70% in 2024.

The EBIT Margin rose from 34% in 2019 to 45% in 2024.

The Net Income grew at a CAGR of 24.58% starting in 2015.

The Free Cash Flow (FCF) Margin increased from 21% in 2015 to 26% in 2024.

The EPS (Earnings per Share) achieved impressive growth from 2015 to 2024, with a CAGR of 26%, increasing from $1,5 to $11,8 per share.

Microsoft's ROA (Return on Assets) has increased from 11% in 2016 to 19% in 2024.

The Return on Equity (ROE) started at 27% in 2016, reached a peak of 47% during the 2021-2022 period, and adjusted to 37% by 2024.

Balance Sheet

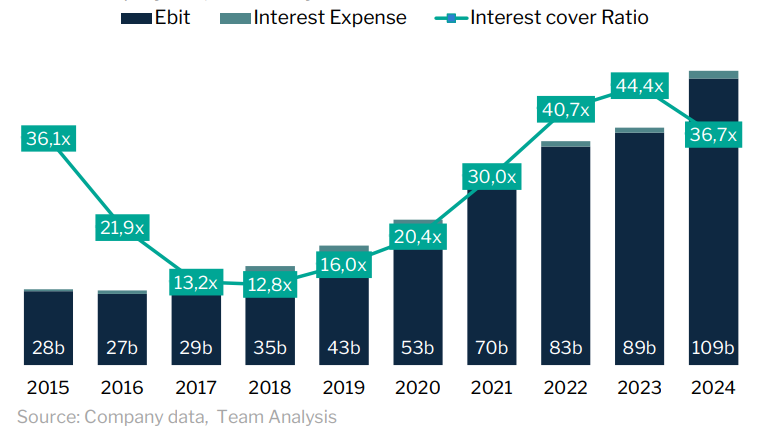

Interest Cover 36,7x

Free-Cash-Flow to debt 0,7x

Quick RAtio 1,1x

Valuation

We use two models to look at the valuation of a company:

Discounted Cash Flows Analysis (DCF)

Relative valuation

DCF

WACC: 8,99%

Terminal growth rate at 4% after 2029

EV/EBITDA multiple of 22,5x

Relative Valuation

Target price of $296 (Downside of 28,7%).

EV/EBITDA 22,9x

The multiples valuation for Microsoft does not align with expectations or the findings from cash flow and DCF analysis. This is because the comparison included smaller companies like SAP, Adobe, Oracle, and IBM, whose business models are similar but whose smaller size results in lower multiples. While Alphabet provided a more comparable benchmark, the overall lower multiples could, without deeper analysis, suggest that Microsoft is overvalued relative to the sector.

Investment risks

Strategic and Competitive Risks

Intense competition in cloud services and AI impacts margins and customer appeal.

Challenges with R&D investments and integrating acquisitions.

Risk of write-offs related to intangible assets.

Cybersecurity and AI Risks

Threats from cyberattacks and data breaches may damage reputation and trust.

Failures in AI innovation could erode competitiveness.

Operational Risks

Service disruptions and supply chain issues affect operational reliability.

Potential hardware defects could harm the brand.

General Risks

Economic pressures and geopolitical tensions pose additional challenges.

Need for talent retention is crucial to sustain

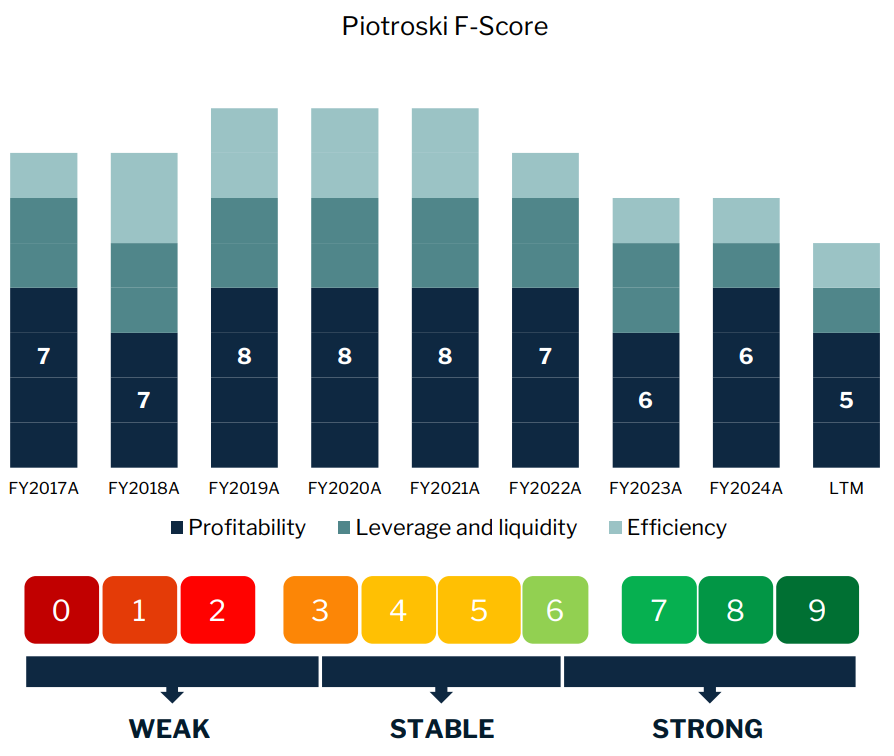

The Piotrosky F-Score

The Piotroski F-Score is a tool used to assess a company's financial health based on nine criteria across three categories: profitability, operational efficiency, and capital structure.

Microsoft’s Piotroski Score in 2024 is within the optimal range of 7 to 9.

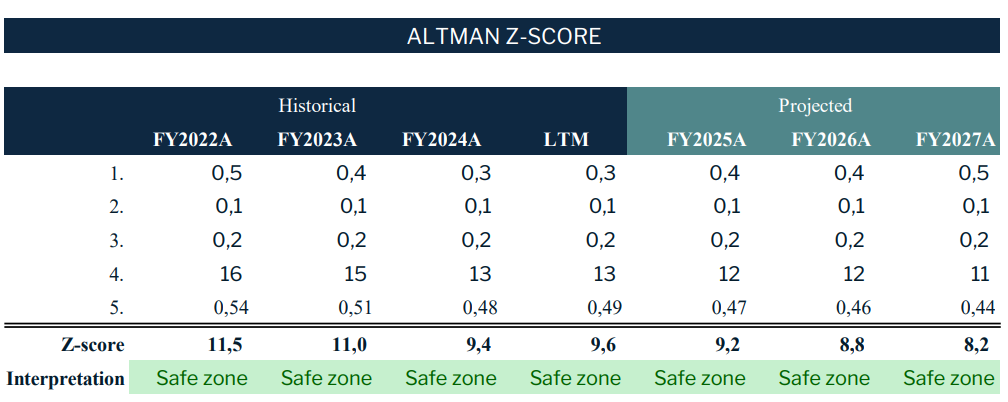

The Altman Z-Score

The Altman Z-score is a financial metric that predicts a company's insolvency risk within two years.

Based on our analysis, the company is in a safe zone, with a low risk of default in the short to medium term.

Final recommendation: we issue a BUY recommendation for Microsoft with a one-year target price of $528.16, presenting a 27.12% upside potential from Microsoft's closing price of $415.49 on November 20th, 2024.

You can access the full research here.